Concern around growth in China and the potential for emerging market (EM) stress has led to increased concern among investors. A recent fund manager survey noted that 75% of participants see a recession in China or an emerging market debt crisis as the most concerning tail risks.

The September Federal Open Market Committee (FOMC) statement addressed the issue with the following comment, “Recent global economic and financial developments may restrain economic activity somewhat and are likely to put further downward pressure on inflation in the near term.”

Why have emerging markets come under pressure?

A combination of structural and cyclical factors has contributed to the downwards pressure on emerging markets:

-

Slowing growth in China.

-

The collapse in commodity prices – negatively impacting the earnings of commodity producers.

-

A decline in trade (hitting those particularly reliant on trade, e.g. Korea and Taiwan).

-

A collapse in currencies, forcing some countries like Brazil and Russia to raise interest rates.

A developing valuation case

Financial vulnerabilities and weakening economic prospects in regions such as Brazil, Russia, South Africa, Turkey and Malaysia are fuelling fears about emerging markets. Currencies in these markets have already fallen significantly and equities are currently falling. This is causing a valuation case for emerging markets to develop. Similarly, emerging market equity funds have seen considerable outflows and many global asset allocators remain significantly underweight in emerging market assets. As such, emerging market equities are likely to rally significantly as prospects turn around. However, things may get worse before they improve.

The developed economies

Developed economies are faring much better than their emerging market counterparts, as the positive domestic dynamics in the major economies, e.g. cheap borrowing costs, cheap oil, and improving labour markets. This has created a positive set of conditions for consumers, which remain a critical part of the major developed economies. With these dynamics expected to continue, a relatively constructive outlook for developed economies is projected.

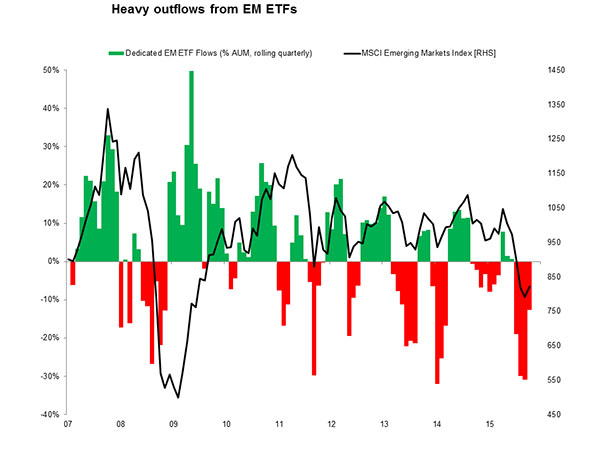

Heavy outflows from dedicated EM ETFs reflect extreme pessimism

Source: AMP Capital, Bloomberg (as of 6 Oct 2015)

With the relative weakness in emerging market growth, shares and currencies developing, things could well get worse before they get better. But given the extreme pessimism and outflows, conditions are ripe for a rebound in emerging market equities.

What does this mean for investors?

The safe bet is to remain cautious and selective when investing in emerging market shares. The structural weaknesses in emerging markets means the bar is high for allocating, but we have a saying that in markets and economics ‘sometimes it’s so bad that it’s good’. So emerging markets look bad right now but for a long-term investor that can be a good thing.

What are the risks? At this point in the cycle conditions are fairly poor and that often means that conditions can either get better or get worse. The downside risks of a continued slump in global trade and commodity prices, the prospect of Fed rate hikes and further weakness in China remain front of mind for emerging markets. However, given the extreme pessimism around China, it may only take some stabilisation in the Chinese economy for emerging markets, and growth assets more broadly, to perform.

Important note: While every care has been taken in the preparation of this article, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) makes no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This article has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this article, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided.